Wallet growth is confidence engineering: how trust becomes repeat use

Wallet growth starts when trust becomes confident action. Learn how utility, usable security, recovery, and first-value design turn adoption into repeat use.

Article Brief

Wallet teams often acquire registrations without creating users who feel confident enough to transact and return.

Growth occurs when utility, usable security, activation, recovery, support, and repeat value operate as one experience.

Better first-transaction conversion, stronger retention, lower support friction, and healthier fraud-adjusted economics.

A wallet can be downloaded in seconds.

That does not mean it has acquired a real user.

The more important moment comes later, when someone is asked to connect a bank account, add a card, submit identity information, fund a balance, protect a recovery method, or approve a transaction involving real money.

That is where wallet growth becomes difficult.

The user is no longer evaluating an advertisement. They are deciding whether the product is reliable enough to become part of their financial life.

This is why wallet growth is not mainly an installation problem. It is a confidence problem.

This builds on a broader principle: wallet growth depends on trust before activation, but confidence engineering extends that principle across first use, recovery, retention, and ecosystem value.

The wallets that grow sustainably do more than persuade people to begin. They help users understand why the product matters, complete a meaningful financial action, recover when something goes wrong, and develop enough confidence to use the wallet again without needing to be resold every time.

In that sense, wallet growth is best understood as confidence engineering.

The wallet market has moved beyond category education

Digital wallets are no longer an unfamiliar edge product.

Worldpay reported that digital wallets represented 56% of global online spending and 33% of in-person spending in 2025. Their role varies by market, but the broader direction is clear: wallets are becoming established payment interfaces rather than speculative alternatives to cards, bank accounts, or cash.

That maturity changes the marketing challenge.

A decade ago, a wallet could attract attention simply by making digital payment possible. Today, a new wallet is more likely to compete against a familiar bank application, an existing payment wallet, a device-native wallet, an exchange account, or a crypto product the user has already learned to navigate.

The question is no longer only:

“Why should I use a wallet?”

It is increasingly:

“Why should I trust this wallet with a financial job I can already perform somewhere else?”

That distinction moves the competitive battleground away from awareness alone.

The wallet must earn preference.

It must demonstrate that it is easier, safer, more useful, more widely accepted, more transparent, or better suited to a specific financial task than the user’s current alternative.

This is where many wallet growth strategies lose their way. They continue to optimize campaigns as though the main obstacle were a lack of traffic. Yet the most damaging friction often appears after the click, when curiosity meets money movement.

The Wallet Confidence Architecture

Confidence begins with a useful reason to change behaviour

Users do not adopt wallets because trust is an abstract virtue.

They adopt them because they expect the wallet to do something valuable.

That may be a faster checkout, a simpler international transfer, access to a stablecoin payout, a better rewards experience, easier entry into an onchain application, greater control over digital assets, or a more convenient way to manage cards, tickets, identity credentials, and payments.

The first layer of confidence is therefore not security. It is value confidence: the belief that learning a new financial behaviour will produce a worthwhile result.

This matters because trust and utility reinforce each other.

A mobile-payment adoption study published in Information Systems Frontiers found perceived benefit and perceived trust to be the strongest influences on intention to adopt. The strategic lesson is not that risk becomes irrelevant. It is that safety without visible utility produces a product people may respect but never use.

A wallet can appear secure and still feel unnecessary.

It can also appear useful and still feel too risky to fund.

Sustainable wallet growth requires both beliefs to exist at the same time:

“This product solves a problem that matters to me.”

And:

“I am sufficiently confident that it will solve that problem without creating a worse one.”

That is why outcome-led messaging is usually stronger than broad innovation language.

The same principle appears across crypto-native positioning strategies that survived market contact: lead with the outcome the audience already values, then explain how the underlying mechanism makes that outcome possible.

“Receive your payout here” gives the user a job to complete.

“Pay with your phone at supported merchants” makes the use case tangible.

“Approve transactions without exposing your private key” translates a security property into a user outcome.

The closer the message is to a real financial job, the easier it becomes for the user to evaluate whether changing behaviour is worthwhile.

The object of trust changes across wallet types

Wallet teams often speak about trust as though it were one universal product attribute.

It is not.

A device-based mobile wallet can borrow confidence from the operating system, the phone manufacturer, the payment network, biometric authentication, and familiar cards already present in the user’s life.

A bank wallet may borrow confidence from regulation, deposit relationships, institutional history, and access to domestic payment rails.

A fintech wallet usually has to prove that the provider can move money reliably, protect the account, explain fees, resolve disputes, and provide support when the normal experience fails.

A custodial crypto wallet asks the user to trust the company’s security, custody model, transaction controls, asset availability, withdrawal processes, and operational resilience. In this case, device security and hygiene is often left in the hands of the user.

A self-custody wallet asks something more demanding.

It asks users to trust the software while also trusting themselves.

They must believe they can protect access, understand approvals, distinguish networks, recognize suspicious requests, recover the wallet, and avoid actions that may be impossible to reverse.

This shift is strategically important.

Traditional financial products often reduce user responsibility by placing more responsibility on the institution. Self-custody products transfer part of that burden back to the user.

The language of ownership may be attractive, but ownership without usable control can quickly feel like liability.

This is why a crypto wallet should not present recovery, transaction previews, signing clarity, and error prevention as peripheral security features. They are part of the growth experience.

Work on usable, trustless decentralized key management reinforces the same principle: preserving self-custody is commercially valuable only when ordinary users can manage access and recovery with reasonable confidence.

An analysis of more than 45,000 mobile cryptocurrency wallet reviews found that both novice and experienced users encountered usability problems capable of causing confusion, disengagement, dangerous mistakes, and irreversible financial loss.

In most consumer software, poor UX creates irritation.

In crypto, it can change the user’s financial outcome.

Usable security is therefore not merely a defensive investment. It influences whether the user reaches activation at all.

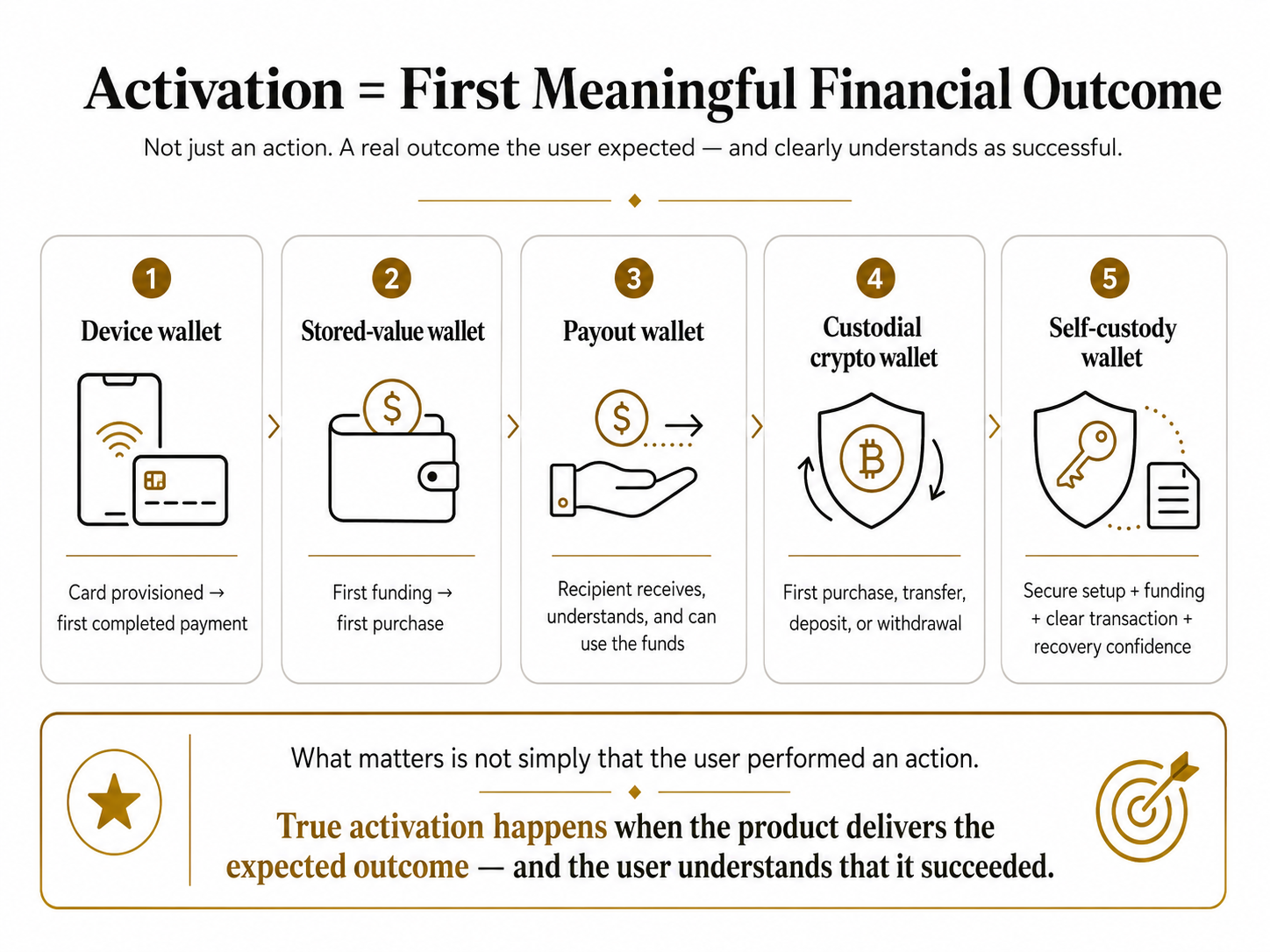

The first meaningful action is where marketing meets product reality

Wallet teams frequently define activation too early.

An account is created.

The verification process begins.

A wallet address is generated.

A card is linked.

A user connects to an application.

These events are useful for funnel analysis, but they do not necessarily mean the wallet has delivered value.

A better activation point is the first meaningful financial outcome.

In Web3 products, the first successful transaction as an activation metric becomes useful only when the action is technically successful, visibly valuable to the user, and predictive of meaningful future behaviour.

For a device wallet, that may be a successfully provisioned card followed by the first completed payment.

For a stored-value wallet, it may be the first funding event and subsequent purchase.

For a payout wallet, it may be the moment the recipient receives, understands, and can use the funds.

For a custodial crypto wallet, it may be the first purchase, transfer, deposit, or withdrawal.

For a self-custody wallet, activation may require secure setup, funding, a clearly understood transaction, and confidence that access can be recovered.

What matters is not simply that the user performed an action.

The product must have delivered the outcome the user expected, and the user must understand that it happened successfully.

This is often where technically functional wallets lose confidence.

The payment completes, but the confirmation screen does not make the result clear.

The transaction lands onchain, but the user cannot find the asset.

The bridge works, but the destination network is unfamiliar.

The recipient receives a stablecoin, but does not understand how to use or redeem it.

The wallet reports that a transaction is pending without explaining what pending means or what the user should do next.

From the system’s perspective, the transaction may be successful.

From the user’s perspective, it may still feel unresolved.

A strong activation experience closes that gap.

It explains what happened, where the value is now, what it cost, whether any further action is required, and what the user can do next.

That reassurance is not decorative copy. It is part of the product outcome.

Security becomes a growth asset when users can see how it helps them

Financial products need strong security whether users understand it or not.

But invisible security and visible confidence perform different jobs.

Invisible controls protect the system.

Visible controls help the user proceed.

The challenge is to make protection understandable without turning every product screen into a technical document.

Good wallet design introduces security at the moment it becomes relevant.

When identity information is requested, the user should understand why it is necessary.

When a bank or card is connected, the wallet should explain how credentials and permissions are handled.

When assets are deposited, the custody model should already be clear.

When a transaction is approved, the user should be able to understand what is being authorized.

When a recovery method is created, the user should understand both its importance and its limitations.

Authentication is a good example of security and growth becoming the same operational problem.

The FIDO Alliance Passkey Index 2025 reported a 93% success rate for passkey sign-ins, compared with 63% for other methods among participating service providers. It also reported materially faster sign-in and an up-to-81% reduction in login-related help-desk incidents.

Those results matter beyond cybersecurity.

A failed login can interrupt onboarding, prevent reactivation, increase support costs, and block a transaction from taking place. Improving authentication can therefore raise conversion while reducing account-takeover exposure and operational friction.

The same principle applies across the wallet journey.

The most valuable security improvements are often those that make the safer action easier to complete than the unsafe one.

Recovery and support determine whether trust survives contact with reality

Most wallet messaging describes the normal experience.

The user will sign up, connect a funding method, transact successfully, and enjoy the product.

Real financial behaviour is less cooperative.

Phones are replaced. Passwords are forgotten. Verification fails. Cards expire. Transactions are delayed. Networks are selected incorrectly. Users encounter scams. Funds appear to be missing. Support is contacted precisely when confidence is at its lowest.

A wallet’s true trust model is revealed during these moments.

This is particularly important because financial users do not judge a product only by what happens when everything works. They also judge it by what they believe will happen when something goes wrong.

That makes recovery, grievance handling, and support part of the growth system.

A study of mobile-payment adoption among 491 consumers in India found grievance redressal to be a significant positive predictor of actual mobile-payment use behaviour.

This is a valuable reminder for marketers: recourse is not only a compliance or customer-service concern. It affects whether users feel safe enough to begin and whether they return after encountering friction.

A user who successfully restores access through a clear recovery process may leave with stronger confidence than before the problem occurred.

A user who receives an opaque support response may abandon the wallet even when the underlying issue is eventually resolved.

The same logic applies to crypto, although the available recourse may be more limited.

A self-custody wallet cannot promise to reverse an irreversible transaction. It can, however, prevent avoidable confusion, make risk legible, improve recovery design, provide transaction simulation, clarify network selection, and help users distinguish between what can and cannot be repaired.

Trust does not require pretending that every mistake can be undone.

It requires being honest about where control and responsibility actually sit.

Incentives can create activity without creating conviction

Wallets operate in a category where incentives are easy to understand and easy to measure.

Rewards could increase registrations.

Cashback offers could generate a first payment.

Referral bonusescould accelerate distribution.

The problem begins when the organization interprets subsidized action as evidence of durable product value.

A large randomized field experiment involving more than 230,000 mobile-app customers found that both monetary incentives and information increased adoption. Monetary incentives created more adopters, but users acquired through information produced more durable downstream purchasing and profit effects.

The experiment was not wallet-specific, so its findings should not be transferred mechanically. The pattern is nevertheless useful.

Some interventions increase the number of people who act.

Others improve the quality of the reason they act.

For wallet teams, this suggests that incentives work best when they help users experience the product’s real utility. A reward attached to a completed first payment, first salary deposit, first successful cross-border transfer, or first repeat transaction can reinforce a valuable behaviour.

A reward attached only to account creation may produce a database rather than a user base.

The distinction appears later in retention.

When the reward disappears, does the financial behaviour remain?

If the answer is no, the promotion rented activity without building confidence, habit, or product preference.

Retention begins when the wallet stops feeling experimental

A first successful transaction is evidence.

A second transaction is a stronger signal.

Over time, repeated success changes the user’s relationship with the wallet. The product moves from something the user is testing to something they expect to work.

This is continuity confidence.

It is created through reliable transactions, predictable fees, understandable records, easier authentication, effective support, safe recovery, and expanding everyday utility.

A post-adoption study of e-wallet users in Jordan found trust to have a strong effect on continuance intention.Trust also influenced expectations about the product’s performance, while continuance intention was connected to continued usage behaviour.

This matters because wallet marketing often becomes less trust-focused after onboarding.

Security appears prominently in acquisition messaging, app-store pages, and trust centres. Once the account exists, lifecycle communication shifts toward offers, promotions, and product announcements.

Yet the post-activation period is when the wallet can create the most convincing evidence.

A transaction confirmation demonstrates reliability.

A fraud alert demonstrates vigilance.

A clear fee breakdown demonstrates transparency.

A successful recovery demonstrates resilience.

A reminder tied to a recurring financial task demonstrates usefulness.

An expansion in merchant or network availability demonstrates growing ecosystem value.

The best retention message is therefore not always “come back.”

It may be:

“Your payment arrived.”

“Your recipient has received the funds.”

“Your card is ready to use.”

“Your recurring transfer is scheduled.”

“Your security settings were updated.”

“This payment method is now supported.”

These communications build confidence because they are connected to something the user is already trying to accomplish.

Wallet growth is also an ecosystem problem

Not every stalled wallet is suffering from an interface problem.

A user may trust the product, complete onboarding, and still find that the wallet is not accepted where they shop.

A recipient may receive funds but lack a convenient way to use them.

This is why recipient onboarding and payment network effects in Web3 are inseparable: a payment network cannot create durable utility when the recipient cannot confidently access, understand, or use the value received.

A bank-linking flow may fail because a financial institution is unsupported.

A crypto wallet may offer excellent UX while lacking the networks, assets, applications, funding methods, or withdrawal routes relevant to the user.

Wallets are often platform products.

Their value depends partly on the number and quality of merchants, counterparties, banks, issuers, networks, applications, and payment methods connected to the system.

This is where consumer funnel analysis becomes insufficient.

Research into digital-payment acceptance among micro, small, and medium-sized retailers found that account ownership, payment infrastructure, mobile-payment applications, fiscal incentives, and market conditions all influence digital-payment acceptance and usage.

A marketing team cannot solve limited acceptance with stronger copy.

A product team cannot solve a relevance problem by shortening a form.

A growth model that looks only at the consumer application will miss the external conditions that make the wallet useful.

For this reason, wallet growth should be measured on both sides.

The team should understand not only whether users complete transactions, but where they can transact, which funding methods succeed, whether recipients become usable participants, and where ecosystem constraints create repeated failure.

Measuring the movement from interest to confident use

Wallet dashboards often give excessive weight to volume.

Installs rise.

Accounts rise.

Monthly active users rise.

Transaction value rises.

These signals are useful, but they do not reveal whether growth is becoming healthier.

A more credible measurement system follows the user’s movement from interest to confident use.

At the beginning of the journey, the team needs to know whether it is attracting people whose needs genuinely match the wallet’s value. That makes qualified traffic, install-to-signup conversion, referral quality, app-store conversion, and fraud-adjusted acquisition cost more useful than raw reach alone.

During onboarding, the central question is where confidence collapses. Verification completion, time to approval, card or bank-link success, passkey enrolment, recovery setup, manual-review rates, false-positive declines, and abandonment by step expose where users become uncertain or operationally blocked.

Activation metrics should then focus on delivered value. First funding, first successful transaction, time to first value, transaction success, first-use support contacts, and progression to a second meaningful action reveal whether the wallet has created a functioning user rather than an administrative account.

Retention should be measured through repeat financial behaviour. Second transaction rate, retained transacting users, recurring-use attachment, active-card behaviour, direct-deposit adoption, repeat funding, and 30- or 90-day value-generating activity provide a more useful picture than return visits alone.

Trust also needs its own instrumentation. Login success, recovery completion, dispute-resolution time, support contacts, transaction abandonment, complaints, false-positive declines, and post-recovery behaviour show whether the wallet’s confidence architecture holds under pressure.

Finally, these outcomes should be connected to economics.

Cost per activated user, incentive cost per retained transactor, support cost, fraud-adjusted lifetime value, and revenue or gross profit per active user help prevent subsidized activity from being mistaken for healthy growth.

The objective is not to create the largest possible dashboard.

It is to understand where confidence becomes behaviour, where behaviour becomes repetition, and where repetition creates business value.

The evidence gives direction, not a universal product recipe

Wallet adoption patterns are remarkably consistent across markets.

Trust, usefulness, security, ease of use, institutional confidence, support, and habit repeatedly appear as important influences.

But teams should be careful about turning those patterns into rigid formulas.

Much of the available evidence is based on cross-sectional surveys, self-reported behaviour, intention measures, and single-country samples. These methods are valuable for identifying recurring relationships, but they are less reliable for predicting the exact growth lift of a new message, feature, or product change.

The relative importance of each factor also changes by market and wallet type.

Government oversight may strongly influence trust in one country. Grievance handling may matter more in another. Merchant acceptance may be the largest barrier in a low-infrastructure market. Recovery comprehension may dominate in self-custody.

The practical response is not to dismiss the broader patterns.

It is to use them as a prioritization map.

Wallet teams can identify likely confidence failures, then test them through funnel analysis, controlled experiments, behavioural data, usability observation, support-ticket analysis, cohort retention, and fraud-adjusted economics.

The framework travels across markets.

The implementation must remain local.

What senior wallet growth strategy should solve

The central growth question is not:

“How do we generate more wallet users?”

It is:

“Where does confidence break, what must the product prove, and which successful action creates a reason to return?”

Answering that question requires marketing to work beyond the campaign surface.

Positioning must clarify the wallet’s real value.

Product must turn the promise into a usable first outcome.

Compliance and risk must protect the system without making the legitimate path unnecessarily difficult.

Lifecycle marketing must help users understand successful activity and discover relevant repeat use.

Support and recovery must preserve confidence when the ideal journey fails.

Analytics must distinguish between activity that looks impressive and behaviour that creates durable economic value.

This is where senior Web3 and fintech growth marketing becomes commercially meaningful.

The role is not to decorate a fragmented experience.

It is to help the organization turn uncertainty into responsible action, and responsible action into repeatable business outcomes.

Wallet, exchange, protocol, and crypto fintech teams experiencing these problems can explore the Web3 Trust & Activation Audit to identify where positioning, onboarding, education, lifecycle communication, or product complexity may be preventing confident usage.

Final takeaway

Wallet growth is not produced by trust alone.

It is produced when trust, utility, usability, recovery, and ecosystem value become one coherent user experience.

The user needs a clear reason to begin.

They need to understand what they are being asked to trust.

They need to complete a meaningful financial action without unnecessary uncertainty.

They need to understand the result.

They need confidence that access, support, and recovery will remain available when the normal journey fails.

And the product must stay useful enough to earn another transaction.

The strongest wallet-growth rule is therefore simple:

Make the valuable path clear, the secure path usable, and the successful path worth repeating.

Frequently Asked

Questions

What is wallet confidence engineering? +

Wallet confidence engineering aligns positioning, onboarding, security, activation, recovery, support, and lifecycle communication so users feel able to complete and repeat meaningful financial actions.

Why is trust alone not enough for wallet growth? +

Trust can make users willing to begin, but the wallet still needs to offer clear utility, usable controls, a successful first outcome, and a practical reason to return.

What should count as wallet activation? +

Activation should normally be the first successful action that delivers the wallet’s core value and has a plausible relationship with continued usage.

Why is crypto wallet growth different? +

Self-custody users must understand recovery, transaction approvals, networks, and potentially irreversible actions. The user must trust both the product and their own ability to operate it safely.

Should wallets use signup incentives? +

Incentives are most useful when they help users experience genuine product value. Rewards tied only to registration can create low-quality acquisition and weak retention.

How can wallet teams measure trust? +

Combine user sentiment with behavioural signals such as login success, recovery completion, transaction abandonment, support contacts, dispute resolution, complaints, and repeat transactions.

Can marketing compensate for weak wallet UX? +

Marketing can clarify value and reduce uncertainty, but it cannot permanently compensate for failed transactions, confusing recovery, limited acceptance, poor support, or unclear fees.

What is the most important wallet-growth metric? +

The first successful value-generating transaction and the rate at which users repeat that action are generally more meaningful than installs or registrations alone.

Author bio

Stefan Furcoi is a senior Web3/Crypto growth marketer focused on wallets, exchanges, protocols, and crypto fintech. His work connects positioning, trust, compliant education, activation, retention, content authority, and measurable business outcomes.

For consulting, advisory, hiring, or collaboration inquiries related to wallet and crypto fintech growth, contact Stefan Furcoi.

Article Disclaimer

The content of this article is provided for general informational purposes only and does not constitute financial, investment, legal or tax advice. StefanFurcoi.com makes no representations or warranties regarding the accuracy or completeness of the information, and it should not be relied upon without consulting qualified professionals. Any views expressed are subject to change and do not reflect any commitment to update the information. You are solely responsible for your decisions and should conduct your own research before acting on any information.