Why wallet growth depends on trust before activation

Wallet growth depends on trust before activation. Learn how crypto wallets, fintech wallets, and payment apps can convert confidence into first use, retention, and revenue-aligned growth.

Article Brief

Wallet growth is a trust-to-activation system, not only an acquisition funnel.

Wallets, exchanges, crypto fintech teams, Web3 apps, and fintech product marketers.

Trust → Onboarding → First Value → Reassurance → Retention → Primacy.

Higher activation, stronger repeat usage, better retention, and clearer growth economics.

Do not scale campaigns before fixing trust, onboarding, and first-use friction.

Show how wallet marketing turns hesitation into trust, activation, and revenue-aligned growth.

Executive summary

Wallet growth is no longer mainly an install problem.

The market already understands the basic wallet behavior. People use digital wallets for checkout, in-store payments, transfers, loyalty, identity, and increasingly for crypto or digital-asset access. The hard part now is not convincing every user that wallets exist. The hard part is convincing the right user that this wallet is safe enough, useful enough, and clear enough to become part of their financial behavior.

That changes the growth strategy.

A wallet does not win because a campaign generated registrations. It wins when users trust the product enough to add credentials, pass verification, fund the account, complete a first meaningful transaction, return for a second use, and eventually make the wallet part of their default money flow.

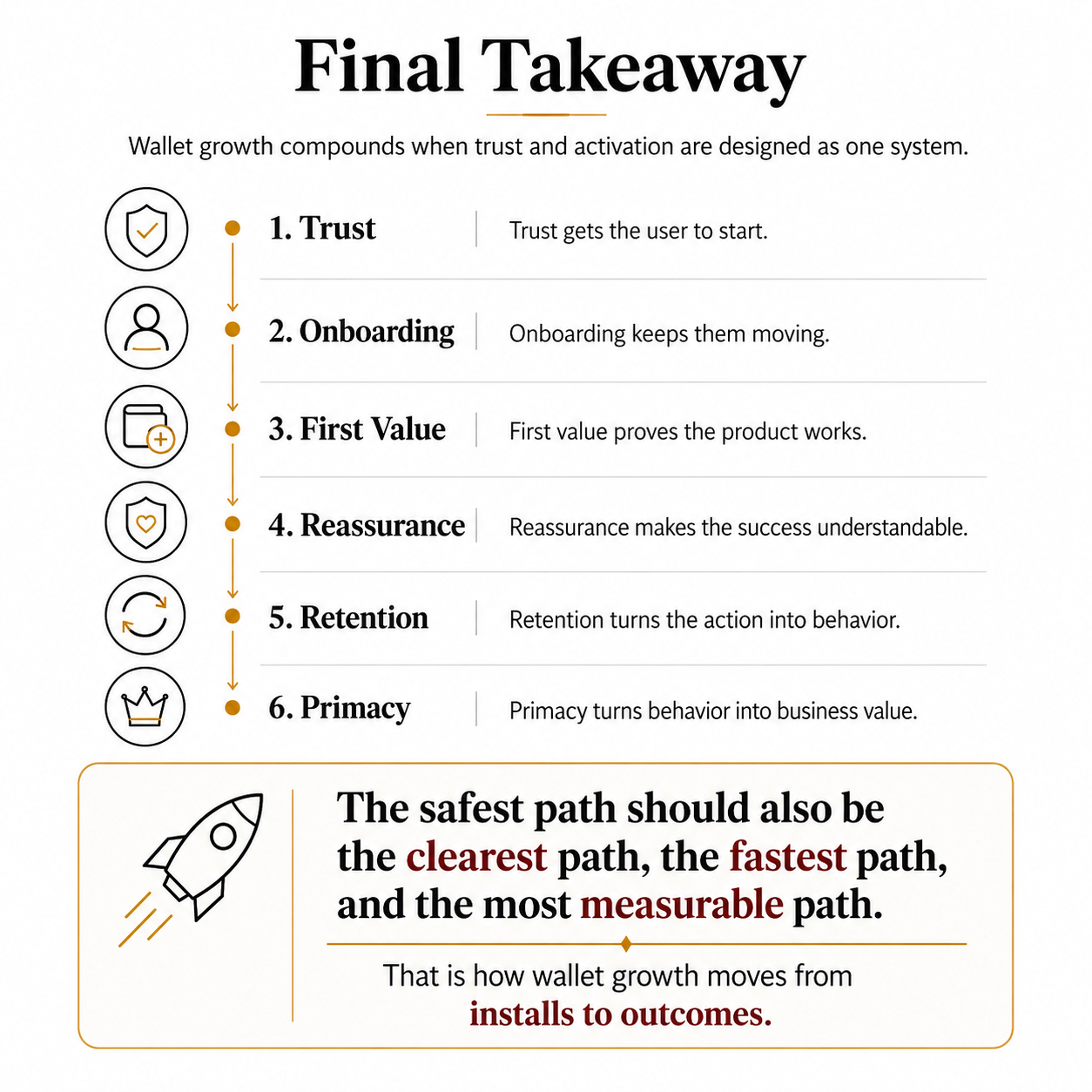

For crypto wallets, exchanges, fintech wallets, and payment apps, trust and activation are not separate workstreams. They are the same system viewed from two angles. Trust gets the user to start. Activation proves the wallet delivered value. Retention shows the experience was good enough to repeat.

The practical growth question is simple:

How do we turn confidence into first value, and first value into durable usage?

Direct answer

Wallet growth depends on trust before activation because users will not add money, payment credentials, identity data, recovery methods, or crypto assets into a product they do not understand or believe is safe. The strongest wallet growth systems reduce fear, compress time-to-first-value, explain security in plain language, and measure success by activated and retained users rather than installs or signups.

For wallet teams, the goal is not just more users entering the funnel. The goal is more users crossing the confidence thresholds that lead to funding, first transaction, repeat usage, account primacy, and revenue-aligned growth.

The problem is not wallet awareness. It is wallet confidence.

Most wallet marketing still behaves as if the main challenge is awareness.

Get more impressions. Drive more installs. Run referral campaigns. Add rewards. Improve app-store screenshots. Push the user into signup.

None of those are useless. The problem is that they are not enough.

A wallet asks for more trust than a normal app. It may ask for identity data, card credentials, bank access, biometric approval, device permissions, crypto keys, recovery setup, or money movement. In that moment, the user is not simply evaluating a feature. They are evaluating risk.

They are asking:

Is this real?

Is my money safe?

Will I lose access?

Will this work where I need it?

Will support help me if something goes wrong?

Is the reward worth the effort?

Is this easier than the product I already use?

For a game, a user can experiment casually. For a wallet, experimentation often feels expensive before any money has moved. That is why wallet growth has a different psychology from ordinary app growth.

The user does not activate because the product exists. The user activates when confidence becomes strong enough to justify action.

What wallet growth actually means

Wallet growth should not be defined as registrations alone.

A registration means the user opened the door. It does not mean they walked into the room, sat down, trusted the host, and decided to come back.

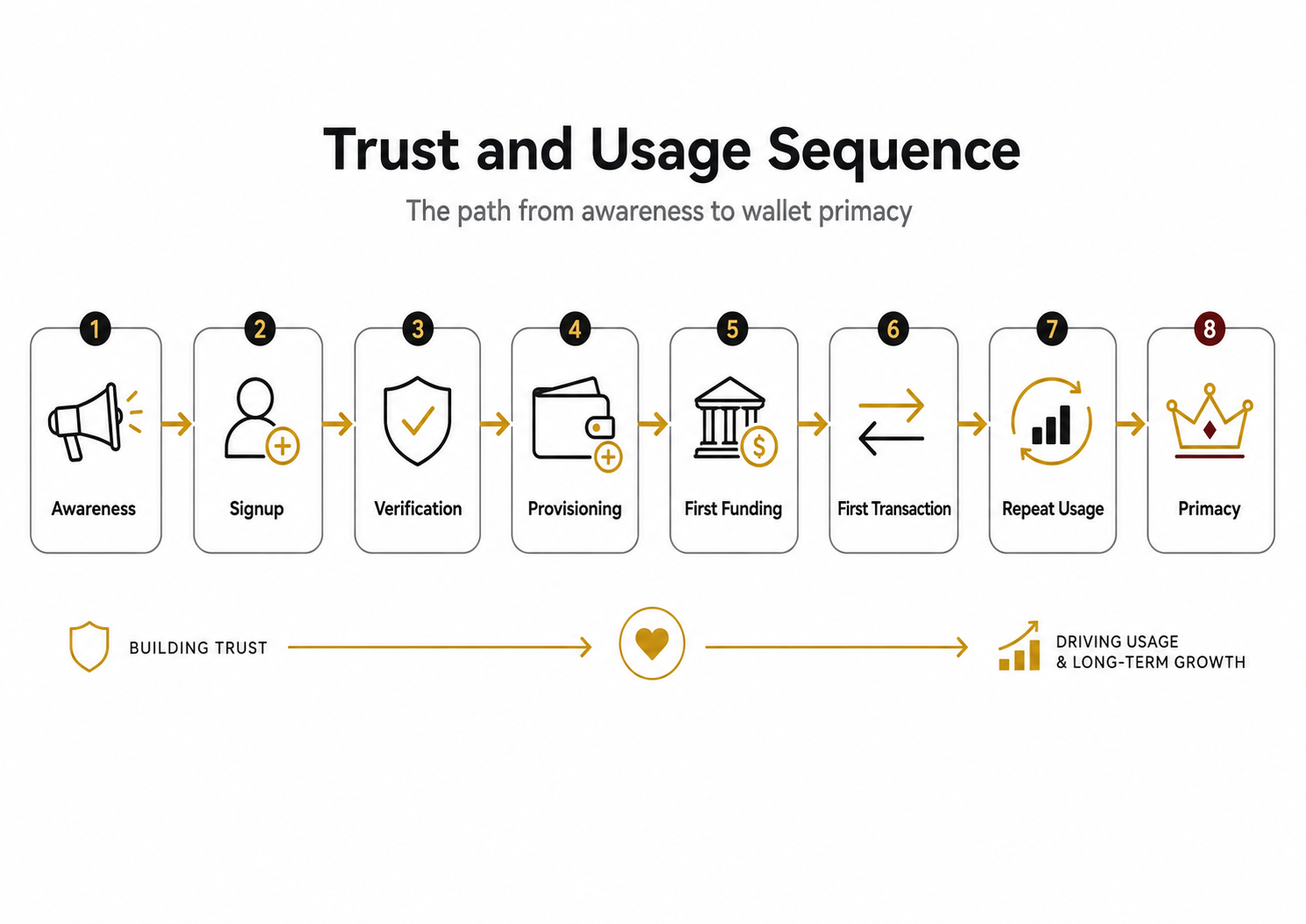

For wallet teams, the more useful definition of growth is movement through a trust and usage sequence:

Each step requires the user to believe something new.

At awareness, they need to believe the wallet is legitimate.

At signup, they need to believe setup is worth the time.

At verification, they need to believe their identity data is handled responsibly.

At card, bank, or wallet provisioning, they need to believe the product will not expose them to unnecessary risk.

At first funding or first transaction, they need to believe the action will complete correctly.

At repeat usage, they need to believe the wallet is dependable.

At primacy, they need to believe the wallet deserves a recurring role in their financial life.

That is why trust-led wallet growth is not soft branding. It is conversion infrastructure.

Why this matters now

Digital wallets have moved into mainstream behavior. This matters because the category can no longer rely only on novelty. When users already understand wallet-like behavior, the competition shifts from category education to trust, convenience, habit, and default status.

Authentication is also becoming a growth lever, not just a security decision. Passkeys and phishing-resistant login experiences matter because every forgotten password, failed login, or suspicious re-entry flow can suppress conversion, monetization, and reactivation. In financial products, login friction is not a small inconvenience. It can stop the user before money ever moves.

At the same time, wallet categories are expanding. A mobile wallet may hold cards, IDs, tickets, loyalty passes, and keys. A fintech wallet may support P2P payments, merchant checkout, bill pay, rewards, and stored value. A crypto wallet may support self-custody, swaps, dapp access, stablecoins, NFTs, or recovery design. A bank wallet may combine payments with account primacy, direct deposit, and local rails.

The shared pattern is obvious: the more valuable the wallet becomes, the more trust it must earn.

A wallet that only asks for attention can grow with ads. A wallet that asks for money, identity, recovery, and repeat usage needs a stronger system.

The wallet trust-to-activation framework

A practical wallet growth system has six layers:

- Trust before signup

- Friction-light onboarding

- First value action

- Post-action reassurance

- Repeat-use retention

- Primacy and reactivation

This framework applies across mobile wallets, e-wallets, bank wallets, crypto wallets, and hybrid products. The exact regulatory and product details will vary by jurisdiction and wallet model, but the operating logic stays consistent.

The user needs confidence before they act.

Then the product must prove the confidence was justified.

1. Trust before signup: earn the right to ask

The first mistake wallet teams make is asking too early.

They ask for the install before explaining the value. They ask for identity before explaining why. They ask for permissions before the user understands the benefit. They ask for funding before the wallet has earned enough confidence.

That may work with a highly motivated user. It usually fails with a cautious one.

Trust before signup is about reducing uncertainty before the user hits the first major commitment point. This is where the landing page, app-store listing, referral copy, paid creative, SEO content, and product screenshots need to do more than describe features.

They need to answer the user’s hidden objections.

For a mainstream wallet user, that may mean showing accepted merchants, device compatibility, bank support, fraud protection language, customer support access, and a simple explanation of what happens next.

For a crypto wallet user, it may mean explaining custody, recovery, supported networks, transaction previews, security controls, scam warnings, and what the wallet can and cannot protect against.

For a fintech wallet, it may mean clarifying verification requirements, account limitations, fees, deposit or transfer timing, supported payment methods, and support paths.

The growth rule is simple:

Do not make users discover the trust story only after they are already nervous.

2. Friction-light onboarding: reduce effort without hiding risk

Onboarding is where many wallet funnels quietly bleed.

The user may have clicked because the promise was strong, but then the product asks for identity, card details, bank linking, device permissions, authentication setup, or recovery choices. Each request can be reasonable. Together, they can feel heavy.

The solution is not to remove every serious step. Wallets operate in environments where security, fraud prevention, compliance, and user protection matter. The solution is to sequence commitment intelligently.

A strong onboarding flow asks for what is needed to unlock the next valuable action, explains why it is needed, and gives the user enough progress visibility to keep going.

This is where progressive verification can matter. A user who only needs to explore the wallet may not need the same flow as a user who wants to fund, trade, withdraw, or transact at higher limits. A user who is adding a card needs different reassurance than a user setting up a self-custody recovery method.

The best onboarding microcopy is not decorative. It removes doubt at the exact moment doubt appears.

“We need this to verify your identity.”

“Your card details are tokenized.”

“You can change this permission later.”

“This recovery method helps you regain access if you lose your device.”

“Verification usually takes a few minutes, but some reviews may take longer.”

That kind of copy is not just UX polish. It is activation support.

3. First value action: define activation correctly

A wallet is not activated when the account is created.

It is activated when the user completes a meaningful first action that predicts future use.

Depending on the wallet, that first value action may be:

- adding and successfully using a card,

- completing a first tap-to-pay payment,

- sending a first P2P transfer,

- receiving a first deposit,

- completing a first bill payment,

- funding the wallet,

- making a first merchant checkout,

- completing a first swap,

- sending a stablecoin payment,

- interacting with a dapp,

- setting up direct deposit,

- or completing a first crypto transaction with clear confirmation.

This matters because teams often optimize the wrong finish line.

If marketing celebrates signups but users never fund, the funnel is not healthy. If a wallet celebrates wallet creation but users never transact, the product has not achieved behavioral adoption. If a crypto wallet celebrates first connection but users never complete a safe transaction, activation is still incomplete.

The first action should be designed like a quality gate.

Did the action complete?

Did the user understand what happened?

Did the product provide confirmation?

Did the user receive the value they expected?

Did the action create a reason to return?

This is where wallet growth becomes more precise. You are not trying to create a generic “user.” You are trying to create a confident user who completed a value-producing action and has a reason to repeat it.

4. Post-action reassurance: do not abandon the user after success

Many wallet experiences treat the confirmation screen as the end.

For the user, it is often the beginning of a new question.

Did it work?

Where did the money go?

Can I reverse it?

What happens next?

When will the recipient see it?

Was there a fee?

Is my balance correct?

Can I use this again?

The post-action moment is one of the most underused trust-building moments in wallet growth. A user who completes a first transaction is emotionally available for reassurance. They are looking for proof that the product did what it promised.

A strong post-action experience should confirm the result, explain what happened in plain language, show where to find the record, provide support access, and guide the next useful action.

For mobile wallets, that may be a clean payment confirmation and merchant record.

For fintech wallets, it may be a receipt, timing explanation, and next-step prompt.

For crypto wallets, it may be a transaction status, network confirmation, fee explanation, asset location, and safety reminder.

For bank-linked wallets, it may be settlement timing, balance update expectations, and dispute guidance.

This is not only support reduction. It is retention design.

A user who understands the first success is more likely to attempt the second success.

5. Repeat-use retention: move from action to habit

Wallet retention comes from habit and primacy.

Habit means the wallet becomes useful for a recurring job. Primacy means the wallet becomes a default financial interface for spending, receiving, storing, moving, or managing value.

A wallet with one successful transaction has proven utility once. A wallet with repeat usage has entered behavior.

That difference matters commercially.

The retention layer should not rely on generic “come back” messaging. Wallet lifecycle marketing needs to be tied to real money jobs.

A user who completed a first payment may need a reminder about accepted merchants.

A user who received money may need an explanation of how to use, withdraw, save, or transfer it.

A user who added a card may need a nudge to make it the default.

A user who completed a crypto swap may need safety education, transaction history clarity, or network-fee guidance.

A user who funded a stored-value wallet may need a reason to repeat the behavior before the balance becomes dormant.

Retention is strongest when the wallet attaches to a recurring context: salary, merchant spend, P2P transfers, bill pay, subscriptions, rewards, travel, gaming, DeFi access, stablecoin payouts, or identity-enabled access.

The marketer’s job is not to create noise. It is to connect the product to the next natural use case.

6. Primacy and reactivation: make return safe and worthwhile

Dormant wallet users often do not behave like dormant media users.

They may not return because they forgot the password, changed devices, lost confidence, saw a fraud headline, failed verification, stopped receiving rewards, or no longer remember what the wallet was for.

That makes wallet reactivation a trust problem before it becomes a campaign problem.

A good winback flow should combine secure re-entry with a specific reason to return.

That reason might be a remaining balance, new merchant acceptance, improved rewards, easier recovery, new local rails, lower friction login, improved security controls, or a clearer use case.

Passkeys and low-friction authentication can be especially powerful here because reactivation often dies at login. A user who wants to return but cannot easily re-enter is not a lost cause. They are a blocked user.

The reactivation message should be serious, sparse, and high-assurance. Financial products do not need gimmicky winback copy. They need verified sender identity, clear language, anti-phishing caution, and a concrete value hook.

The goal is not to beg the user to come back.

The goal is to make returning feel safe, useful, and worth the effort.

What wallet teams usually get wrong

The first mistake is scaling acquisition before fixing trust leakage.

A wallet can buy traffic all day, but if users abandon at verification, bank linking, passkey enrollment, first funding, or first transaction, the campaign is only feeding a broken system faster.

The second mistake is measuring account creation as activation.

A wallet account without first value is not growth. It is potential energy sitting in the database.

The third mistake is treating security as a separate page instead of a conversion layer.

Users do not only care about security when they visit the Help Center. They care about it when they add a card, connect a bank, approve a transaction, set up recovery, or move money.

The fourth mistake is using one message for every wallet user.

A crypto-native user, a mainstream mobile-wallet user, a merchant, a fintech customer, and a cautious beginner do not need the same trust sequence.

The fifth mistake is treating incentives as a substitute for confidence.

Rewards can move behavior, but they cannot compensate for fear, unclear value, poor onboarding, failed payments, or weak support.

The sixth mistake is separating marketing, product, risk, compliance, and support.

Wallet growth touches all of them. If those teams are not aligned, the user feels the fragmentation.

What to do instead

Start by mapping the wallet journey as a series of confidence thresholds.

Where does the user hesitate?

Where do they abandon?

Which step asks for the most trust?

Which explanation is missing?

Which support ticket keeps appearing?

Which successful action predicts retention?

Which activation event produces meaningful business value?

From there, the growth work becomes much more practical.

For acquisition, lead with the trust trigger that matters most to the segment. That may be safety, convenience, acceptance, speed, self-custody control, account protection, lower friction, or merchant coverage.

For onboarding, reduce unnecessary branching and explain each sensitive request. Do not let users feel surprised by verification, card linking, device permissions, recovery setup, or transaction limits.

For activation, design one fastest path to first value. If the user came for a first payment, guide them there. If they came to receive funds, guide them there. If they came for a first crypto action, make the safe path obvious.

For retention, build lifecycle flows around money jobs rather than generic engagement. A wallet is not a social feed. “You haven’t opened the app” is usually weaker than “Your card is ready to use,” “Your transfer completed,” “Your recurring payment can be set up,” or “Your security settings are updated.”

For reactivation, fix re-entry before writing clever copy. A user who cannot log in, recover access, or understand what changed will not be persuaded by a discount.

This is the senior wallet growth principle:

Make the secure path the easiest path.

How to measure wallet growth properly

A serious wallet-growth dashboard should separate volume, quality, trust, risk, and economics.

At acquisition, measure cost per qualified signup, install-to-signup rate, referred share, branded search demand, app-store conversion, and trust-message performance.

At onboarding, measure signup completion, identity start, identity pass rate, time to verify, add-card success, bank-link success, wallet-provisioning success, passkey enrollment, permission acceptance, and drop-off by step.

At activation, measure first funding, first transaction, payment success, time to first value, day-one activation, day-seven activation, first-transaction fraud rate, and first-use support tickets.

At retention, measure weekly active users, monthly active users, repeat-transaction frequency, second transaction rate, 30-day retention, 90-day retention, direct-deposit attach, card active rate, inflows per active, and share-of-wallet proxies.

At trust and safety, measure login success, account takeover rate, false-positive declines, dispute rate, chargeback rate, support contact rate, complaints per active user, and security-center engagement.

At economics, measure gross profit per active user, cost per activated user, incentive cost per retained user, fraud-adjusted LTV, CAC payback, and reactivation cost per revived transactor.

The important distinction is this:

Weak wallet marketing stops at attention.

Strong wallet marketing connects attention to trust, trust to activation, activation to retention, and retention to durable economics.

The wallet growth experiments worth prioritizing

The best experiments are not always the loudest campaigns.

Often, the highest-impact tests are the ones that reduce fear or compress the path to first value.

A strong first experiment cluster could include:

- passkey-first login versus password-first login,

- progressive verification versus full verification upfront,

- “why we ask” microcopy during identity or bank-linking steps,

- first real transaction incentive versus signup bonus,

- security-led acquisition copy versus convenience-led copy,

- first-use tutorial length,

- confirmation-screen reassurance,

- post-transaction next-step prompts,

- wallet default-setting nudges,

- and secure winback flows for dormant users.

Notice the pattern. These experiments do not treat growth as only demand generation. They treat growth as user confidence engineering.

That is where wallets can find hidden lift without pretending every problem is a media-buying problem.

A useful distinction: trust does not mean more friction

There is one important nuance.

Trust-led growth does not mean making everything slower, heavier, or more compliance-theater-heavy.

A wallet can be secure and still feel unusable. A wallet can have serious controls and still explain them poorly. A wallet can ask for legitimate verification and still lose users because the flow feels opaque.

Trust is not the same as friction.

Trust is confidence.

Sometimes confidence comes from stronger authentication. Sometimes it comes from fewer steps. Sometimes it comes from better explanations. Sometimes it comes from better recovery. Sometimes it comes from showing the user exactly what will happen before they approve an action.

For crypto wallets, this nuance matters even more. Hiding complexity can damage trust with advanced users. But dumping complexity on beginners can kill activation. The right answer is progressive clarity: simple enough to start, transparent enough to trust, detailed enough for users who need depth.

Good wallet growth does not remove every hard thing.

It puts the hard thing in the right place, at the right time, with the right explanation.

What this means for crypto wallets and exchanges

Crypto wallets and exchanges face a sharper version of the same problem.

The user may be worried about scams, irreversible transactions, seed phrases, lost access, network fees, custody, regulatory uncertainty, phishing, support quality, or simply pressing the wrong button.

That means crypto wallet marketing cannot stop at “easy self-custody,” “secure trading,” or “simple onboarding.”

Those claims need proof inside the journey.

A crypto wallet growth system should explain custody clearly, show transaction previews, make network and fee choices understandable, offer safer recovery paths where appropriate, identify risky interactions, and confirm outcomes in language the user understands.

For exchanges, the same logic applies to funding, verification, first trade, withdrawal, education, risk controls, support, and lifecycle retention.

The marketer’s role is not only to get the user to click.

It is to help the product earn enough confidence for the user to take the next responsible action.

That is why compliant education matters. It is not filler content. It is part of activation infrastructure.

Commercial bridge

For wallets, exchanges, and crypto fintech teams, the practical question is not only “How do we acquire more users?”

The better question is:

Where are users hesitating, what proof do they need, and how should the funnel turn trust into first value, repeat usage, and revenue-aligned growth?

That is the level where wallet marketing becomes more than campaign execution. It becomes a system connecting positioning, onboarding, lifecycle messaging, product trust signals, support readiness, compliance sensitivity, and measurement.

A wallet team that understands this can spend more intelligently, onboard more responsibly, and build user behavior that survives beyond the first promotion.

Frequently Asked

Questions

What is wallet growth through trust and activation? +

Wallet growth through trust and activation is a strategy that helps users move from interest to confident first use, repeat usage, and long-term retention. It focuses on reducing fear, explaining sensitive steps, improving onboarding, guiding the first meaningful transaction, and measuring outcomes beyond signups.

Why is trust important for wallet activation? +

Trust matters because wallets often ask users to share identity data, add payment credentials, connect bank accounts, manage recovery, store value, or move money. Users are unlikely to complete those actions unless the product feels safe, clear, and useful.

What counts as wallet activation? +

Wallet activation should usually be defined as the first successful value action, not account creation. Depending on the wallet, this may be first funding, first payment, first P2P transfer, first tap-to-pay transaction, first bill payment, first crypto send, first swap, first deposit, or first dapp interaction.

How should wallet teams measure trust-led growth? +

Wallet teams should measure signup completion, verification pass rate, add-card success, bank-link success, passkey enrollment, login success, first-transaction rate, time to first value, repeat usage, retention, support tickets, dispute rates, fraud-adjusted LTV, and cost per activated user.

What do wallet teams usually get wrong? +

Wallet teams often scale acquisition before fixing onboarding friction, define activation as signup, hide trust information in support pages, use one message for every user segment, rely too heavily on incentives, and separate marketing from product, compliance, risk, and support.

How does this apply to crypto wallets? +

Crypto wallets need to earn confidence around custody, recovery, transaction approval, network fees, scam prevention, supported assets, and safe first use. The best crypto wallet growth systems simplify the first action while keeping security, recovery, and risk explanations visible when users need them.

Are incentives useful for wallet growth? +

Incentives can be useful when they are tied to high-quality actions such as first funding, first transaction, recurring use, or direct deposit. They are weaker when they reward vanity registrations without improving activation, retention, or unit economics.

Author note

Stefan Furcoi is a senior Web3/Crypto growth marketer focused on wallets, exchanges, protocols, and crypto fintech. His work connects positioning, trust, compliant education, activation, retention, content authority, and measurable business outcomes.

Article Disclaimer

The content of this article is provided for general informational purposes only and does not constitute financial, investment, legal or tax advice. StefanFurcoi.com makes no representations or warranties regarding the accuracy or completeness of the information, and it should not be relied upon without consulting qualified professionals. Any views expressed are subject to change and do not reflect any commitment to update the information. You are solely responsible for your decisions and should conduct your own research before acting on any information.